It wasn’t always that the big banks of the world had so much power.

But these days, for every $1 invested in local credit unions, there is $14 dollars invested in the big broad institutional banks. The total market share for credit unions is just over 1 trillion USD while big banks these days account for a staggering 14.5 Trillion dollars. JP Morgan alone has more $ in assets than all US credit unions combined by nearly double.

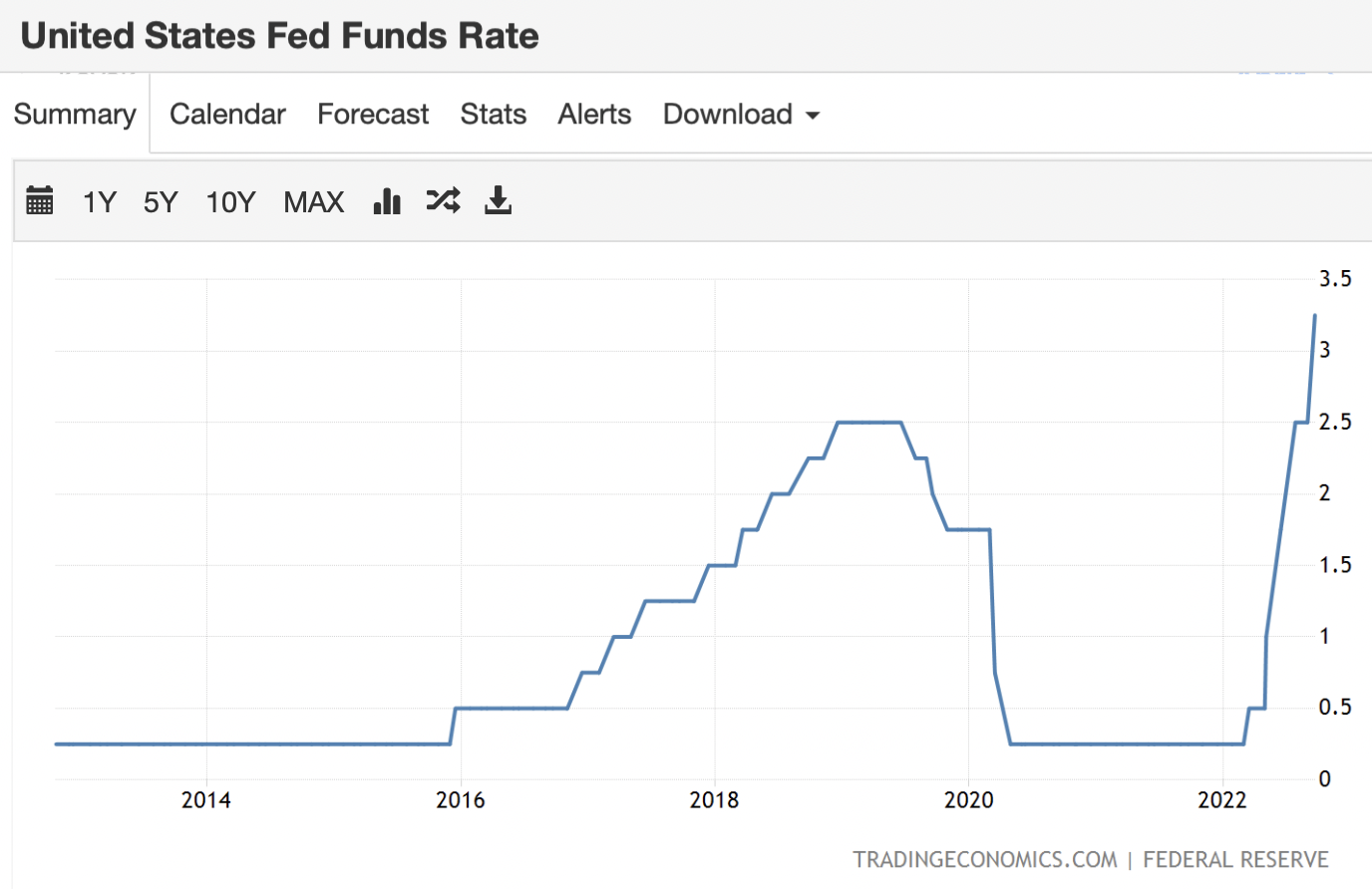

The US (and world) housing market is facing unprecedented times. Last year a never before heard of $13 trillion was injected into the United States economy in just 1 year ($5.2T for COVID + $4.5T for Quantitative Easing + $3 for infrastructure). Between 2020 and 2021 the FED printed more dollars than ever before in history. We are now facing the effects of some of this decision making.

In order to combat rapid inflation in the housing market, federal interest rates have been raised to higher levels than anything seen in the previous decade. Some are predicting that the Fed will raise the interest rates to 4.25 – 4.5% before the end of the year.

Small businesses across the country have been forced to close their doors and send faithful employees home.

So how are credit unions able to survive in this environment despite their small 5-6% share of the market? How can they continue to compete?

Well there’s lots of perks to working with a credit union over a large financial institution. One perk is that they are going to spend more time attending to your accounts. In general, they are known for their customer service.

They are also more affordable for smaller clients. Where a larger bank may charge a fee for opening up an account or charge you if your account dips below a certain level, credit unions usually let you open your account for free and waive any fees that make the poor poorer.

The Future of Credit Union Banking

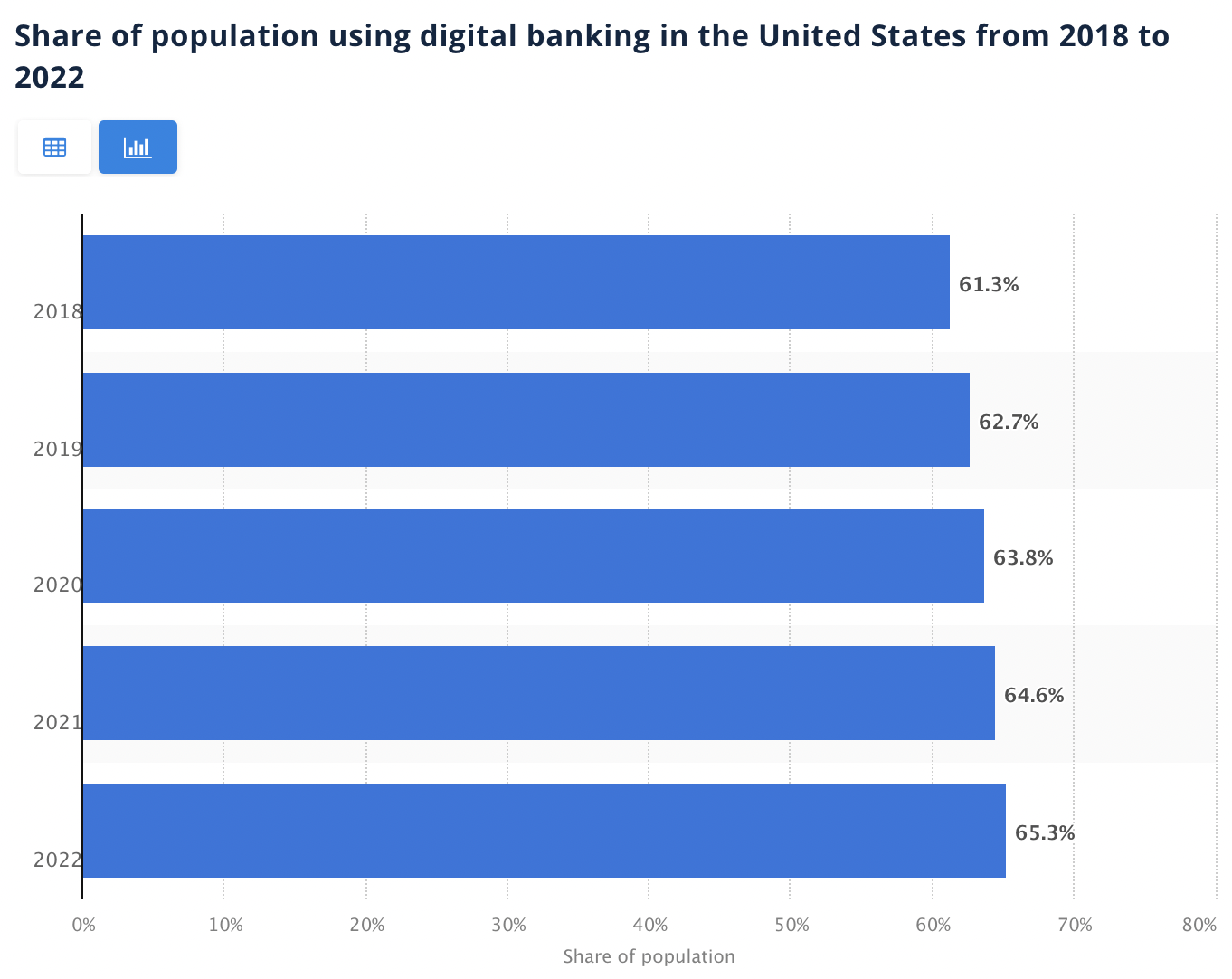

As everyone adjusts to a new post-covid world, more and more banking has moved online. Over This 65% of Americans are using digital banking in the year of 2022 and this number does not show any sign of going down as baby boomers and millennials move up the ol age brackets.

This means the credit unions that want to compete will need to adapt and build an online presence without having the same huge budget to throw at developers that large institutions might. People would prefer to check the bank account balance from the comfort of their home rather than drive down to the bank and who can blame them?

Checking your balance and paying bills aren’t the only thing that you can do on the internet. As of 2014 in Virginia (and really since the start of Covid) people have been able to conduct necessary notarizations for their legal docs online. Now, you can get legal docs notarized from your home just as easy as you can view your checking account balance.

One way that credit unions can compete in this aspect without having a heavy budget is to partner up and outsource their notarizations and loan closings through a notarization platform like BlueNotary. They can even integrate this Remote Online Notarization API with their own domain. This allows them to offer the same premiere services to their clients that the big dogs in the space do.

How a Credit Union Can Keep up with The Joneses

There are a variety of reasons a credit union or even a major bank should take advantage of a Remote Online Notarization platform.

- The #1 reason a client should partner with a RON platform is INCREASED CUSTOMER SATISFACTION. Over 75% of people prefer banking online. Only the oldest age brackets will still prefer to get in the car and drive down to the bank.

- The 2nd most important reason is that it saves both you and your customer time. This frees up more time to run and grow your credit union through other means, and your client will never be upset about you saving them time.

- Thirdly, you will have much lower cost in regards to administrative costs like mailing hard copies of documents. With RON, customers can access their documents from anywhere in the world anytime. Our platform also stores your notarization and even the video of the session for 10 years.

- Lastly, credit unions can benefit from signing up from Online Notarization by increasing the security of EACH notarization. More high tech security measures simply mean less fraud as an end result. Save worry and headspace with KBA and biometric authorization.

Simply put, online notarization creates ease and efficiency for the entire credit union or bank. Banks no longer have to spend time certifying or training their notaries and they no longer need to worry about balancing their staff and ensuring someone capable of providing notarizations is in the office at all times or as much as possible.

The average bank branch costs $600,000 – $800,000 per year to run and that’s not including the initial $2-4 million required just to open a new location. Banks and credit unions are constantly trying to improve efficiency and productivity in order to compete and survive with significant costs. This means everything from who they staff to decreasing operational costs must be accounted for and analyzed with judicial scrutiny. Occasionally, budget cuts must be made, especially in times of rampant inflation.

To increase profits, credit unions would be wise to include online notarizations in their offerings. This is something that can be featured on their website and it will enhance the experience of their customers. The credit union can start to save money on notary commissions, training, and E & O insurance on a large scale while their customers are left impressed and thankful.

How else can a credit union save money on staffing as well as increasing customer satisfaction? It’s a win-win situation. Customers have proven that they are ready for digital banking and all its perks. We’re ready to help you deliver exactly what your customer wants and we can do it by saving everybody money.

Curious about what it would take to bring your credit union or bank into the new world of modern day finance?

Learn more by signing up for a demo now.