If you want to have any shot at lowering your closing costs, you first have to know what you're looking at. The real strategy is to get your hands on that closing statement, figure out which fees are coming from the lender versus a third party, and then zero in on the ones you can actually negotiate. A lot more of them are flexible than most people realize.

Decoding Your Closing Cost Statement

Before you can start trimming the fat, you need a clear map of where your money is going. The closing cost statement—which you'll first see as a Loan Estimate and later as the final Closing Disclosure—can look like it's written in another language. It's just a long, intimidating list of fees, taxes, and prepayments that all seem to blur together.

But getting a handle on this document is the single most important thing you can do to save some cash.

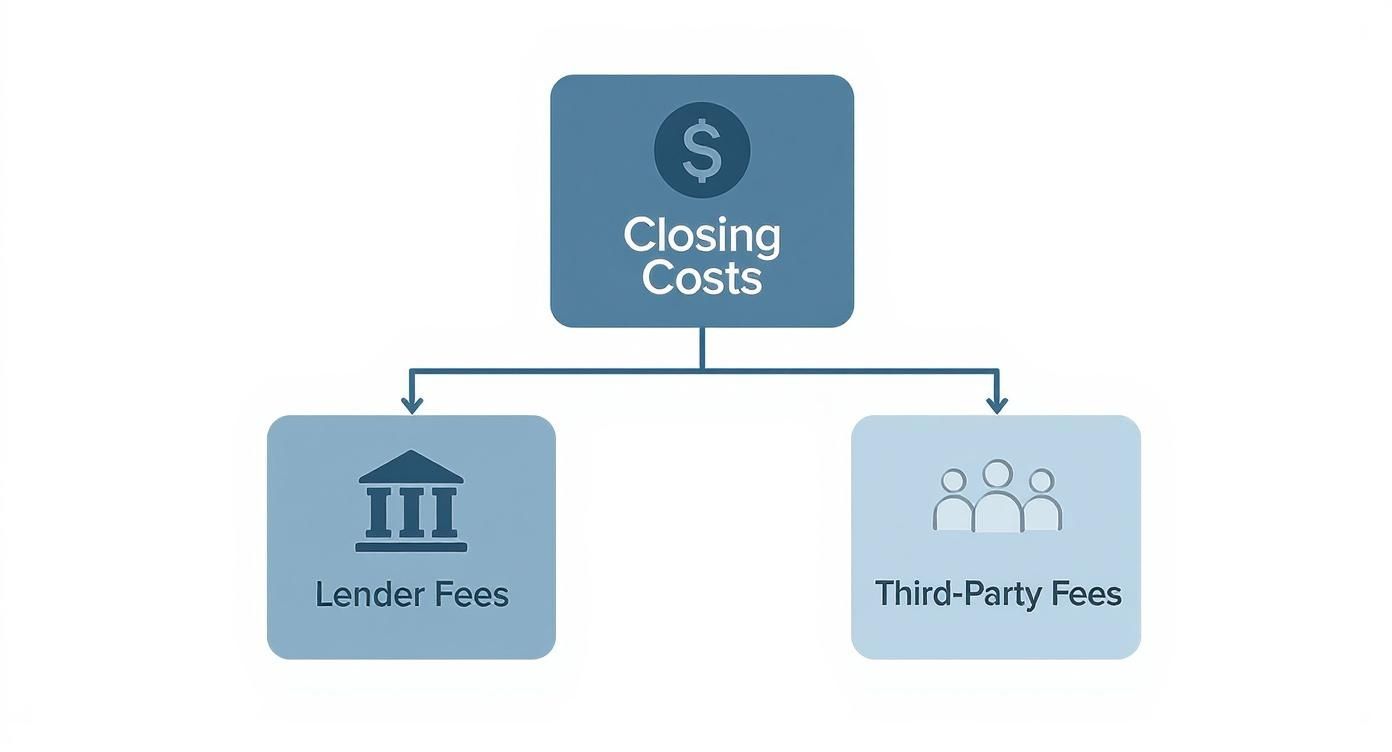

It helps to think of closing costs in two main buckets: lender fees and third-party fees. Lender fees are what the bank charges for the loan itself. Third-party fees are for all the other pros who have to get involved, like appraisers and title companies. The secret to reducing your closing costs is knowing which fees in each bucket have wiggle room.

This visual gives you a good breakdown of the two main categories, helping you see where your money is really going.

Once you separate the lender fees from the third-party charges, you can focus your energy where it'll actually make a difference.

Lender Fees: What You Can Influence

Lender fees are directly controlled by the bank or mortgage company funding your loan. This is where you'll find the most fertile ground for negotiation because the lender has total discretion over these charges.

- Origination Fee: This is the lender’s fee for processing your application. It’s often a percentage, like 1%, of your total loan amount.

- Underwriting Fee: The cost for the lender to dig into your finances and decide if you're a good risk.

- Application Fee: An upfront charge to cover the administrative work to get your loan file started.

- Discount Points: This is prepaid interest you can buy to lock in a lower mortgage rate. While you choose to pay this, the cost per point isn't always set in stone.

None of these fees are non-negotiable. When you have multiple loan offers, you can play them against each other. Use a lower fee from one lender as leverage and ask another if they can match or beat it.

Third-Party Fees: Where You Can Shop Around

Third-party fees are paid to outside companies for services needed to get the deal done. Your lender might have a list of "preferred" providers, but you're rarely stuck with them. A little comparison shopping here can lead to big savings.

These costs cover crucial steps in the homebuying process, including payments into a neutral holding account. If you want to learn more about how that works, you can check out our detailed guide on https://bluenotary.us/what-does-it-mean-to-be-in-escrow.

Common third-party fees include:

- Title Insurance: This protects you and the lender from any old claims against the property's title. You have the right to shop around for a title company.

- Appraisal Fee: Pays a licensed appraiser to confirm the home's market value for the bank.

- Home Inspection Fee: Covers a professional inspection to uncover any hidden problems with the house.

- Attorney Fees: If required in your state, this covers the legal review of all the paperwork.

Key Takeaway: You have the right to shop for most third-party services. Don't just go with your lender's suggestions without getting at least two other quotes.

To help you get a better sense of what's what, here's a quick breakdown of common fees and whether they're typically fixed or open to negotiation.

Common Closing Costs Breakdown Fixed vs Negotiable

| Fee Type | Typical Cost Range (% of Loan) | Negotiability | Who It Pays |

|---|---|---|---|

| Origination Fee | 0.5% – 1.5% | Negotiable | Lender |

| Underwriting Fee | $300 – $1,000 (Flat Fee) | Negotiable | Lender |

| Appraisal Fee | $300 – $600 | Shop Around | Appraiser |

| Title Insurance | 0.5% – 1.0% | Shop Around | Title Company |

| Home Inspection | $300 – $500 | Shop Around | Inspector |

| Property Taxes | Varies by location | Fixed | Government |

| Recording Fees | $125 – $250 | Fixed | Government |

| Attorney Fees | $500 – $1,500+ | Shop Around | Attorney |

As you can see, plenty of these line items have some flexibility if you're willing to do a little homework.

Understanding how much these costs can swing is key. Back in 2021, the national average for closing costs on a single-family home was $6,905, but that number hides some massive regional differences. For instance, costs in Washington, D.C., were nearly $29,888 on average, while in Missouri, the average was just $2,061.

This just goes to show how much local market conditions and provider rates can affect your final bill. For sellers, exploring ways to sell your home without agent fees or closing costs can also be a game-changer. These huge variances prove that there's real money to be saved if you're willing to scrutinize the numbers.

Finding Savings by Shopping for Lenders and Services

One of the most powerful moves you can make to slash your final bill is to treat the home buying process like any other major purchase—you’ve got to comparison shop. Too many buyers get tunnel vision, focusing only on the lowest interest rate. But that’s just one piece of the puzzle. The real savings are often buried in the lender’s fees and the costs for third-party services.

When you apply for a mortgage, federal law requires every lender to give you a standardized Loan Estimate form within three business days. This document is your secret weapon. It’s designed for a true apples-to-apples comparison, so don’t just glance at the interest rate. You need to dive into the details, especially the charges the lender directly controls.

Scrutinize Lender-Specific Fees in Section A

The first page of your Loan Estimate is where the action is. Look for Section A: Origination Charges. This is where lenders list the fees they charge for the privilege of giving you their money. These fees are not set in stone and can vary wildly between institutions.

This is your prime negotiation territory. Keep an eye out for these line items:

- Application Fee: Some lenders charge this just to look at your paperwork. Others don't.

- Origination Fee: Often a percentage of the loan amount (think 0.5% to 1.5%), this is a major profit center for lenders and is highly negotiable.

- Underwriting Fee: This covers the cost of having a professional underwriter comb through your finances to approve the loan.

Once you have a few Loan Estimates in hand, make a simple chart comparing these Section A fees. If Lender A is charging a $900 underwriting fee but Lender B is only charging $400, you’ve found your leverage. Call Lender A and ask them to match or beat the competition. In a competitive market, many are willing to trim these charges to win your business.

Insider Tip: Don't be afraid to ask a lender to waive the smaller "junk fees" like "processing" or "document preparation" charges. A simple, polite request is often all it takes to get these knocked off, saving you a few hundred bucks.

You Have the Right to Shop for Third-Party Services

Your Loan Estimate also lists costs for services from other companies, like title insurance, pest inspections, and surveys. Your lender will hand you a list of their preferred vendors, but here's a critical detail many homebuyers miss: in most cases, you are not required to use them.

Shopping around for these services can unlock some serious savings. For example, title insurance premiums can differ by hundreds of dollars between companies for the exact same policy. Get quotes from at least two or three different providers for each service. For real estate pros looking to make this part of the transaction smoother, knowing what tech and partners are available to lenders can give you a major competitive advantage.

To make sure you're getting a clear picture, have a few key questions ready for each vendor you call.

Questions to Ask When Shopping for Services

- Can you give me a detailed, itemized quote? You want a full fee schedule, not just a headline number. A title company might quote a low premium but then load up the back end with high "settlement" or "document" fees.

- Do you offer any bundled discounts? Some title companies have a "reissue rate" if the property has a recent policy. Others might give you a break if you use them for both the title search and the settlement.

- What’s your timeline for getting this done? A cheaper provider isn't a good deal if they cause delays that put your closing date at risk. Make sure they can meet your deadlines.

- Are your fees negotiable? While things like government recording fees are fixed, many administrative or ancillary charges are not. It never, ever hurts to ask.

Making a few extra phone calls can easily save you $500 to $1,500 or more on these third-party costs. It’s a tiny investment of your time for a huge return, leaving more cash in your pocket when you get the keys.

Negotiating Seller Concessions to Your Advantage

Shopping for lenders and services is smart, but one of the most direct ways to slash your closing costs is through simple, powerful negotiation. I'm talking about seller concessions. This is a common and highly effective strategy where you ask the seller to contribute funds toward your closing costs, meaning you need less cash to get your keys on closing day.

Think of it this way: the cost essentially gets rolled into your loan without you having to finance it directly. Let's say you agree on a $400,000 purchase price but are facing $8,000 in closing costs. You could offer $408,000 for the home while asking the seller for an $8,000 credit. The seller still walks away with their target of $400,000, and you get to avoid a massive out-of-pocket hit.

This isn’t just a neat trick; it's a standard practice in real estate that can make or break a deal. The key is knowing how to frame the request.

Gauging Your Negotiating Power

Your ability to successfully negotiate seller concessions almost always comes down to the temperature of the real estate market. You have to know if it's a buyer's market or a seller's market to keep your expectations in check.

- In a Buyer's Market: When there are more homes for sale than active buyers, you're in the driver's seat. Sellers are often more motivated and willing to negotiate to get their property sold. In this climate, asking for reasonable concessions is pretty standard—some sellers even expect it.

- In a Seller's Market: When inventory is tight and homes are flying off the market, sellers hold all the cards. Asking for concessions could make your offer look weaker next to one that doesn't. You might have to offer a bit more on the purchase price to compensate for your request or find other areas to negotiate.

Understanding this dynamic is step one. A great rule of thumb? If a home has been sitting on the market for 60 days or more, your odds of a successful negotiation go way up, no matter what the broader market looks like.

How to Craft a Compelling Offer

When you ask for seller credits, the goal is to create a win-win. You aren't asking for a handout; you're just structuring the deal differently to help with your cash flow while still hitting the seller's number. Your agent should weave this into the offer from the start, not tack it on as an afterthought.

Here’s the kind of language you'll often see in an offer addendum:

"Buyer requests a seller credit of 3% of the purchase price to be applied toward buyer's recurring and non-recurring closing costs, prepaid items, and any lender-allowable fees."

This phrasing is boilerplate for a reason—it’s clear and covers just about every closing-related fee. Make sure the amount you request is specific and justifiable, ideally matching up with the estimated costs on your Loan Estimate.

And don't forget the seller's side of the equation. Their biggest closing cost is usually the real estate commission. For sellers looking to maximize their net profit, selling your home without a real estate agent is an attractive option that can save them thousands, potentially making them more flexible on things like concessions.

Know the Lender Limits on Contributions

While negotiating is a fantastic tool, lenders have firm rules about how much a seller can kick in. These limits exist to prevent buyers and sellers from artificially inflating home values. If you ask for too much, your loan will get flagged and likely rejected, so you absolutely must know the caps for your loan type.

These limits are set as a percentage of the home's sale price:

| Loan Type | Maximum Seller Contribution |

|---|---|

| Conventional Loan (Less than 10% down) | 3% of the sale price |

| Conventional Loan (10% – 25% down) | 6% of the sale price |

| Conventional Loan (More than 25% down) | 9% of the sale price |

| FHA Loan | 6% of the sale price |

| VA Loan | 4% of the loan amount (plus standard closing costs) |

| USDA Loan | 6% of the sale price |

Before you even write the offer, double-check the exact limit for your specific situation with your lender. This simple step ensures your negotiated credit is well within the guidelines and won't throw a wrench in your financing at the last minute.

These rules aren't arbitrary. Research on FHA loans, for example, found that capping seller concessions was a critical move to reduce risk in the mortgage system. While helpful for buyers, high concessions were linked to higher default rates. The FHA's decision to cap them was estimated to slash net losses by $60 to $70 million annually. You can read the full research about these FHA policies to see the bigger picture. It's a clear reminder of why staying within these established limits is so important for a smooth, stable transaction.

Using Strategic Timing to Lower Your Fees

Timing really is everything in real estate, and that old cliché extends right to your wallet on closing day.

Most homebuyers don't think about when they sign their final paperwork, but the date on that calendar can have a real, tangible impact on how much cash you need to bring to the table. This isn't about trying to time the market—it’s about understanding how certain fees are calculated and using that to your advantage.

One of the simplest and most effective tactics is scheduling your closing for the end of the month. The reason comes down to a line item that often gets overlooked: prepaid interest.

Here’s the deal: when you close, you have to pay the interest that will build up on your mortgage for the rest of that month. Your first official mortgage payment isn't due until the first of the next month. So, if you close on the 5th of a 30-day month, you're on the hook for 26 days of per diem interest at closing. But if you close on the 29th? You only owe for a single day.

The End-of-the-Month Advantage

This small scheduling tweak can make a huge difference, especially with today's loan amounts. It’s a well-known trick, so closing dates at the month's end can get snapped up quickly. It's smart to talk to your lender and real estate agent about locking in a date as early as you possibly can.

Let's break down a real-world example:

- Loan Amount: $400,000

- Interest Rate: 6.5%

- Daily Interest (Per Diem): About $71.23

If you close on the 10th of the month, you'd owe for 21 days of prepaid interest. That's $1,495.83 out of pocket.

Now, let's say you close on the 28th. You’d only owe for three days, which comes to just $213.69. That’s a savings of nearly $1,300 in cash you get to keep in your bank account.

This timing trick doesn't reduce the total interest you'll pay over the life of the loan, but it significantly cuts the amount of upfront cash you need at closing, which is often the biggest hurdle for buyers.

Scheduling During Off-Peak Times

Beyond the end-of-the-month scramble, think about the time of year. The real estate market has its seasons. Spring and summer are notoriously busy, meaning lenders, title companies, and appraisers are slammed. When they're in high demand, they have zero incentive to negotiate their fees or offer competitive pricing.

If you have the flexibility, scheduling your closing during the slower months—think late fall or the winter lull between holidays—can sometimes work in your favor. With less business coming in, some of those third-party providers might just be a little more flexible on their rates. It’s not a guaranteed discount, but every little bit helps.

Locking in Your Interest Rate at the Right Moment

Finally, one of the most critical timing moves you can make is when you lock in your interest rate. This decision can save you thousands over the life of your loan. Rates move up and down every single day based on what the market is doing.

A rate lock is simply a promise from your lender to hold a specific interest rate for you for a set period, usually 30 to 60 days.

Locking in protects you from a sudden rate hike that could jack up your monthly payment. You'll want to work closely with your loan officer on this, keeping an eye on the market trends. If rates are climbing, locking in early gives you peace of mind. If they're bouncing around or dropping, you might be tempted to wait, but that's a gamble. Nailing that sweet spot is a crucial part of knowing how to reduce closing costs in the long run.

Scrutinizing Your Closing Disclosure for Hidden Savings

The Closing Disclosure, or CD, is the final, most critical document you'll see before the keys are in your hand. Federal law isn't kidding around here—it requires your lender to get this document to you at least three business days before you’re scheduled to sign. This isn't just a formality. It’s your last real chance to spot costly mistakes and question any charges that look fishy.

Think of the CD as the final, itemized bill for your home. Your one job during this three-day window is to compare it, line-by-line, against the Loan Estimate you got at the very beginning. Any big differences between these two documents are red flags you need to raise immediately.

The Loan Estimate vs. Closing Disclosure Showdown

When you sit down with both documents, your entire focus should be on hunting for unexpected fee increases. Some costs are allowed to change a little, but others are legally locked in. Lenders have to follow strict rules, called "tolerances," that limit how much certain fees can jump from the estimate to the final bill.

Here’s where to zero in:

- Zero Tolerance Fees: These costs absolutely cannot increase. Not even by a penny. This includes fees paid directly to the lender or mortgage broker, like their origination fee, application fee, and any discount points you paid to get a better interest rate.

- 10% Tolerance Fees: This bucket of third-party fees can’t go up by more than 10% in total. We’re talking about things like recording fees and required inspection services where you used a provider your lender recommended.

- Unlimited Tolerance Fees: Some costs can change without any limit, but only in specific situations. This typically includes things like your prepaid interest, homeowners insurance premiums, and any fees for services you shopped for yourself (meaning you didn't use the lender's suggested vendor).

If you see a brand-new "document prep fee" that wasn't on your Loan Estimate, that’s not a legitimate change. It's an error, and you have every right to challenge it.

In hot real estate markets, these "small" discrepancies can add up to serious money. In California, for example, seller closing costs can average around 2.72% of the sale price. On a $572,000 home, that's nearly $15,600. With fixed costs like property taxes taking a huge bite, the fees you can reduce are usually service charges—the exact items you need to be double-checking on your CD. You can dig deeper into these California closing cost breakdowns on listwithclever.com.

To help you with this crucial review, here is a simple checklist for comparing your Loan Estimate and Closing Disclosure.

Closing Disclosure Review Checklist

Before you sign anything, use this table to systematically compare your two most important loan documents. This process is your final opportunity to catch errors that could cost you hundreds or even thousands of dollars.

| Checklist Item | Loan Estimate Section | Closing Disclosure Section | What to Look For |

|---|---|---|---|

| Loan Terms | Page 1 | Page 1 | Confirm Loan Amount, Interest Rate, and Monthly Payment match exactly. |

| Projected Payments | Page 1 | Page 1 | Verify that Property Taxes and Homeowner's Insurance estimates are consistent. |

| Loan Costs | Page 2, Section A | Page 2, Section A | Origination Charges (origination, application, underwriting fees) must NOT increase. |

| Services You Cannot Shop For | Page 2, Section B | Page 2, Section B | The total of these fees (appraisal, credit report, etc.) cannot increase by more than 10%. |

| Services You Can Shop For | Page 2, Section C | Page 2, Section C | If you used the lender's provider, the 10% tolerance limit applies. If you chose your own, fees can vary. |

| Taxes & Government Fees | Page 2, Section E | Page 2, Section E | Check Recording Fees. These are subject to the 10% tolerance rule. |

| Prepaids | Page 2, Section F | Page 2, Section F | Ensure your Homeowner's Insurance and Prepaid Interest calculations are correct. |

| Cash to Close | Page 1 | Page 1 | The final "Cash to Close" figure should be very close to the estimate, minus your earnest money deposit. |

This line-by-line review is non-negotiable. Take your time, ask questions, and don't let anyone rush you through it.

How to Question and Correct Errors

Spotting an error is just the first step. Now you have to get it fixed. Don't feel intimidated—this is your money, and questioning fees is a routine part of the business for lenders and title companies.

Your first call should be to your loan officer. Be polite but firm.

Here’s a simple script to use:

"Hi [Loan Officer's Name], I'm looking at my Closing Disclosure and see the underwriting fee is $950. On my original Loan Estimate from [Date], it was listed as $600. Could you explain this increase and have it corrected to match the estimate?"

This approach is non-confrontational and puts the ball in their court to justify the charge. Most of the time, legitimate mistakes are fixed pretty quickly once you point them out. These final checks are more important than ever as closings move online. For a closer look at this shift, read about our dirty little eClosing secret.

If you get any pushback, don't be afraid to escalate the issue to the closing agent or a manager at the mortgage company. Just remember, the closing can't happen without your signature. That gives you a ton of leverage to make sure the numbers are right before you sign on the dotted line.

Still Have Questions About Closing Costs?

Even with the best strategies laid out, you're bound to have some specific questions pop up. Let's be honest, navigating the world of closing costs can feel like learning a new language, filled with jargon and scenarios that are anything but straightforward. This section is all about tackling the most common questions I hear from buyers and sellers, giving you clear, direct answers so you can walk into closing day with confidence.

We'll cover everything from getting the seller to chip in to the real story behind "no-closing-cost" mortgages. Think of this as your personal cheat sheet for those final, lingering uncertainties.

What Is a Closing Cost Credit and How Do I Ask for It?

A closing cost credit, which you'll often hear called a seller concession, is simply an agreement where the seller pays for a portion of your closing costs. It's a fantastic tool because it directly lowers the amount of cash you need to bring to the table on closing day. You aren't actually getting a discount on the home's price; you're just structuring the deal to finance these upfront fees into the total loan.

So, how do you get one? You have to ask for it as a formal part of your initial offer. Your real estate agent will write a clause specifying the amount you're requesting. This can be a flat dollar figure or a percentage of the purchase price (like 3%). The real key is to make the request reasonable and base it on current market conditions—you'll have a lot more leverage in a buyer's market.

Are "No-Closing-Cost" Mortgages a Good Deal?

A "no-closing-cost" mortgage sounds almost too good to be true, and it's critical to understand the trade-off. In reality, those costs don't magically vanish. The lender covers them for you, but in exchange, you agree to a higher interest rate on your loan for its entire term.

This can be a smart play if you're a bit short on cash for closing but can comfortably handle the slightly higher monthly payment. Over the long haul, though, you will almost certainly pay more in total interest.

Pro Tip: Do the math on your break-even point. Figure out how many months it will take for the savings from your higher monthly payment to equal the closing costs you skipped. If you plan to sell or refinance before you hit that point, the no-closing-cost option might just be a winner for you.

Can I Roll Closing Costs into My Loan?

Yes, this is another popular way to reduce how much cash you need upfront. It works a lot like a no-closing-cost mortgage, but instead, you're adding the closing costs directly to your total loan principal. From there, you'll finance them over the life of the mortgage, which is usually 15 or 30 years.

This move increases both your total loan amount and your monthly payment. While it definitely makes getting into the home more accessible from a cash-flow perspective, remember that you'll be paying interest on those rolled-in costs for decades. It's a strategic choice that prioritizes immediate cash savings over long-term cost.

Can Improving My Credit Score Lower Closing Costs?

Absolutely, though it's more of an indirect benefit. A higher credit score won't magically reduce fixed fees like the appraisal or title search. Where it really helps is by directly impacting the biggest costs tied to your mortgage itself.

A better credit score is your ticket to a lower interest rate, which is the single biggest long-term saving you can score. On top of that, it can lower your private mortgage insurance (PMI) premium if your down payment is less than 20%. Some lenders even offer better terms on their own origination fees to highly qualified borrowers. Boosting your score by just 20 points before you apply can unlock some pretty substantial savings.

What Happens if I Can’t Afford Closing Costs at the Last Minute?

Finding yourself short on funds right before closing can be stressful, but don't panic. You just need to act fast. Here are a few options:

- Request a gift: A family member can often provide a gift to cover the gap. Your lender will just need a formal gift letter confirming the money is not a loan that needs to be repaid.

- Go back to the seller: It's a long shot, but you might be able to renegotiate for a seller credit, especially if a new issue popped up during the final walkthrough.

- Check assistance programs: Quickly look into state or local first-time homebuyer programs. Many offer grants or low-interest loans specifically for closing costs.

The most important thing is to communicate with your lender and real estate agent immediately. They've seen it all before and can help you explore viable solutions to make sure the deal doesn't fall apart.

Ready to transform your closing process from a marathon of paperwork into a sprint? At BlueNotary, our secure eClosing and online notarization platform helps lenders, title companies, and real estate professionals close deals in under 45 minutes. Reduce errors, save over $450 per transaction, and provide a seamless experience for your clients. Discover how BlueNotary can streamline your closings today!